“It’s not brilliance. It’s just

avoiding stupidity.”

Warren Buffet’s 60-year investing partner, Charlie Munger, has famously said this more than once about the astonishing success of Berkshire Hathaway over 60 years. But what comprises stupidity? Is it one-time foolishness or a pattern of dumb?

A reckless mistake, or a poorly devised strategy, or just a bad habit? Can someone of average intelligence achieve truly impressive

investment returns?

A reckless mistake, or a poorly devised strategy, or just a bad habit? Can someone of average intelligence achieve truly impressive

investment returns?

In truth, the list of “don’t’s” in stock investing is

probably longer than the list of ”do’s”. But they’re both more intuitive and

less technical in a lot of ways. Which means they’re more accessible to regular

folks who have never studied finance or who have crazy schedules and simply

can’t put in the time to nail the details. Which is to say, if you can just

avoid touching the third rail, you’ll probably do fine.

probably longer than the list of ”do’s”. But they’re both more intuitive and

less technical in a lot of ways. Which means they’re more accessible to regular

folks who have never studied finance or who have crazy schedules and simply

can’t put in the time to nail the details. Which is to say, if you can just

avoid touching the third rail, you’ll probably do fine.

Don’t invest in

mutual funds.

mutual funds.

I go into more depth on this subject in another

post, but I’ll nutshell it here: if after reading all my investing how-to

you still feel like you aren’t ready to pick your own stocks, get yourself an

online brokerage account at E*Trade

or TD

Ameritrade and pick up a couple of ETFs (exchange traded

funds), which hold a basket of companies but trade as a single stock. The

easiest are the large-basket ETFs like VOO and SPY, which mimic the

movement of the largest market index of 500 different stocks. If instead you

insist on paying a professional fund manager to hand-pick stocks for a mutual

fund, you’ll pay 1-2% of your assets for that manager’s

‘expertise’—which frequently does not outperform your own common sense—and your

money will be much less liquid should you need to access it. The vast majority

of mutual funds do no better than the broader market and you pay for the

privilege. Don’t believe me? Read this

and this,

by other people.

post, but I’ll nutshell it here: if after reading all my investing how-to

you still feel like you aren’t ready to pick your own stocks, get yourself an

online brokerage account at E*Trade

or TD

Ameritrade and pick up a couple of ETFs (exchange traded

funds), which hold a basket of companies but trade as a single stock. The

easiest are the large-basket ETFs like VOO and SPY, which mimic the

movement of the largest market index of 500 different stocks. If instead you

insist on paying a professional fund manager to hand-pick stocks for a mutual

fund, you’ll pay 1-2% of your assets for that manager’s

‘expertise’—which frequently does not outperform your own common sense—and your

money will be much less liquid should you need to access it. The vast majority

of mutual funds do no better than the broader market and you pay for the

privilege. Don’t believe me? Read this

and this,

by other people.

Don’t worry about the

price of a share.

price of a share.

Lots of people get weirded out by the cost per share. They

think that if a share is $500 and they can only afford one share, better to

find something for $100 per, or $20 per share and buy more shares. Which is

ridiculous: if you’re going to spend the same dollar amount, and the company is

going to rise, say, 10% in the next year, then you’re 10% wealthier either way.

Go with the company which best fits your investment model and your interests.

think that if a share is $500 and they can only afford one share, better to

find something for $100 per, or $20 per share and buy more shares. Which is

ridiculous: if you’re going to spend the same dollar amount, and the company is

going to rise, say, 10% in the next year, then you’re 10% wealthier either way.

Go with the company which best fits your investment model and your interests.

The other thing that happens is that people avoid companies analysts

describe as “overvalued,” whose shares have risen substantially over recent

months. The thinking is that if it’s gone up that much it’s probably close to

tapped out, and the price will flatten or even fall. But the truth is, no

matter what analysts say, that stock’s price has risen because investors

overall have decided it’s worth a lot more than previously thought. Perhaps the

company acquired a competitor, or

announced some international expansion, justifying the rise. If instead you only buy

stocks that you think are undervalued or “on a dip,” you miss out on some

amazing opportunities (think Apple, Amazon, Netflix). Companies with rising

valuations tend to keep rising until something changes—a new competitor, a

corporate scandal, an economic shock. If

you stop worrying about how high the price looks today, and measure it instead against the potential for that

business tomorrow, you’ll have a much clearer understanding of the future value, which

is why you want to own it in the first place.

describe as “overvalued,” whose shares have risen substantially over recent

months. The thinking is that if it’s gone up that much it’s probably close to

tapped out, and the price will flatten or even fall. But the truth is, no

matter what analysts say, that stock’s price has risen because investors

overall have decided it’s worth a lot more than previously thought. Perhaps the

company acquired a competitor, or

announced some international expansion, justifying the rise. If instead you only buy

stocks that you think are undervalued or “on a dip,” you miss out on some

amazing opportunities (think Apple, Amazon, Netflix). Companies with rising

valuations tend to keep rising until something changes—a new competitor, a

corporate scandal, an economic shock. If

you stop worrying about how high the price looks today, and measure it instead against the potential for that

business tomorrow, you’ll have a much clearer understanding of the future value, which

is why you want to own it in the first place.

Don’t buy blind.

When you hear from a friend or a trusted broker about a

great value stock or a sudden opportunity that “won’t last long,” your inclination is to believe they know something

you don’t and therefore you should jump. But it ought to be a red flag: if you’re hearing about it from

someone else, the likelihood is you’re not already following that business, or

you would already know this information. (Plus, if word has already gotten

around, then any amazing momentary price is likely already over.) Don’t succumb

to the temptation to get in with your friend just because. Do a little research.

Understand what the business does, who their competition is, what kind of

leadership they have, how their growth trajectory looks. Get a feel for things.

If you don’t understand how the company makes money today and how big the opportunity is the future, how can you possibly assess it as an investment? You’re buying an ownership stake in an ongoing business: you’re

much more interested in where they’re going than where they are or where

they’ve been.

great value stock or a sudden opportunity that “won’t last long,” your inclination is to believe they know something

you don’t and therefore you should jump. But it ought to be a red flag: if you’re hearing about it from

someone else, the likelihood is you’re not already following that business, or

you would already know this information. (Plus, if word has already gotten

around, then any amazing momentary price is likely already over.) Don’t succumb

to the temptation to get in with your friend just because. Do a little research.

Understand what the business does, who their competition is, what kind of

leadership they have, how their growth trajectory looks. Get a feel for things.

If you don’t understand how the company makes money today and how big the opportunity is the future, how can you possibly assess it as an investment? You’re buying an ownership stake in an ongoing business: you’re

much more interested in where they’re going than where they are or where

they’ve been.

Don’t be in a hurry.

Unlike in the movies, investing is not shorting orange juice

futures one time and finding yourself on a yacht in the Bahamas for the rest of

your life. Investing is a lifelong process. It requires an understanding that the

value of your assets will rise and fall in in the near term but, with patience,

will likely increase substantially over time.

futures one time and finding yourself on a yacht in the Bahamas for the rest of

your life. Investing is a lifelong process. It requires an understanding that the

value of your assets will rise and fall in in the near term but, with patience,

will likely increase substantially over time.

A lot of people succumb to action

bias, which is just the need to do

something with your investment

portfolio beyond just watching it grow. Because most folks don’t have an endless supply of incoming cash

with which to buy more or different stocks, they instead move the money they

have from one investment to another, looking for higher or faster returns. This

eliminates any one business’s ability to earn them a substantial return over

time, it kills the stunning advantage brought by compounding interest, it generates capital gains taxes and transaction fees, it takes time and energy

and increases frustration. Instead, buy smart and sit tight: investing, not

trading. Your returns will demonstrate the difference.

bias, which is just the need to do

something with your investment

portfolio beyond just watching it grow. Because most folks don’t have an endless supply of incoming cash

with which to buy more or different stocks, they instead move the money they

have from one investment to another, looking for higher or faster returns. This

eliminates any one business’s ability to earn them a substantial return over

time, it kills the stunning advantage brought by compounding interest, it generates capital gains taxes and transaction fees, it takes time and energy

and increases frustration. Instead, buy smart and sit tight: investing, not

trading. Your returns will demonstrate the difference.

Don’t let your

emotions take over.

emotions take over.

Investing well, and I’ve said this before here,

Investing well, and I’ve said this before here,and here,

requires a steady hand on the helm and your eyes on the horizon. There’s just

no way around it. Stocks rise over time, but in the shorter term they gyrate

all over the place and some of it is just plain sickening. This is especially

true of young companies, technology companies, and of so-called “fad”

companies, whose products or services might turn out to be just a momentary

cultural obsession (think Sodastream, GoPro, Crocs, Tesla) which analysts and

investors worry will fade in time. If you act on your emotions, you might save

yourself a headache or a sleepless night but over time you will have terrible

returns. Never buy on a whim of fancy, and never sell in a panic. (There are

exceptions, but you’ll know them when you see them—like Volkswagen.) Buy it with some

thought and analysis and some vision, then then sit on your stocks for years.

That’s it. Containing yourself is certainly hard, but it’s not complicated.

Don’t sell on movement.

Everyone sets out to buy low and sell high. But the reality

is often very different: we buy high (see “Don’t worry about the price,” above)

and sell when it drops because we fear it will keep dropping. Clearly, this will prove a poor strategy over time.

is often very different: we buy high (see “Don’t worry about the price,” above)

and sell when it drops because we fear it will keep dropping. Clearly, this will prove a poor strategy over time.

Once you own shares, don’t sell unless you must. I go into

Once you own shares, don’t sell unless you must. I go intomuch greater detail in When

to Sell, but the basic idea is that, if you did at least a little due

diligence prior to purchase, and you still like the company and believe in

their capacity to grow, then you shouldn’t sell just because it has moved up

or down. Stocks swing, sometimes a lot, and sometimes very quickly. Selling

because it’s dropped substantially following a missed quarterly earnings report

(a Wall Street analyst’s problem, not the company’s or the shareholder’s

problem)— or worse, because it popped upwards, is exactly the kind of behavior

you want to avoid. You bought it to hold it, expecting it would slowly move

up— so let it. Sell only when something really bad has happened at the company

(again: Volkswagen) or when you need the money for something else. Trust your

purchase, trust your judgment. Patience is rewarded.

Don’t wait.

You’ve been hearing it since you landed your first job, if not earlier: the longer you put off the start of your investing career, the less

You’ve been hearing it since you landed your first job, if not earlier: the longer you put off the start of your investing career, the lesstime you’ll have to earn enough to stop working.

0

0

1

1447

8251

Zaga Investment Co

68

19

9679

14.0

Normal

0

false

false

false

EN-US

JA

X-NONE

/* Style Definitions */

table.MsoNormalTable

{mso-style-name:”Table Normal”;

mso-tstyle-rowband-size:0;

mso-tstyle-colband-size:0;

mso-style-noshow:yes;

mso-style-priority:99;

mso-style-parent:””;

mso-padding-alt:0in 5.4pt 0in 5.4pt;

mso-para-margin:0in;

mso-para-margin-bottom:.0001pt;

mso-pagination:widow-orphan;

font-size:12.0pt;

font-family:Cambria;

mso-ascii-font-family:Cambria;

mso-ascii-theme-font:minor-latin;

mso-hansi-font-family:Cambria;

mso-hansi-theme-font:minor-latin;}

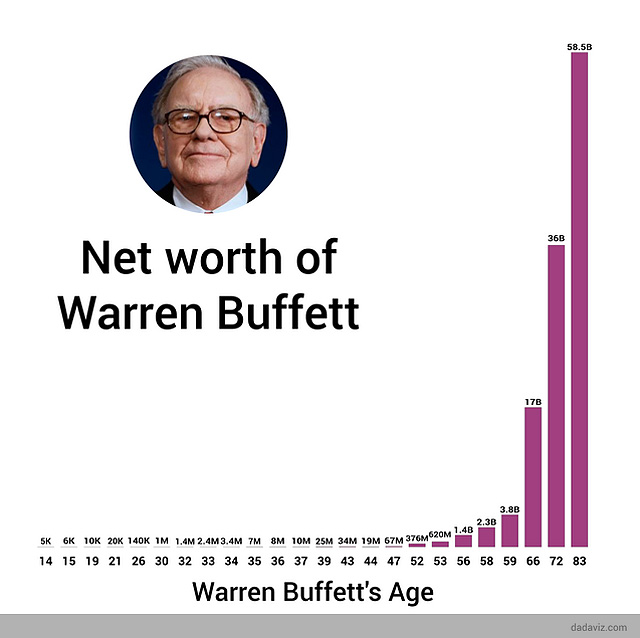

Take a look at this chart of Warren Buffett’s personal

wealth. Can you see the huge hockey-stick shape to the right? His net worth

grows steadily enough over time but really accelerates in the last decade or

so? That’s compounding interest. I keep saying it: the longer you do it, the

faster you’ll earn and the more you’ll have. Investing is the slow boat, so get

on now. For more on the subject of waiting to get started, have a look at

this.

wealth. Can you see the huge hockey-stick shape to the right? His net worth

grows steadily enough over time but really accelerates in the last decade or

so? That’s compounding interest. I keep saying it: the longer you do it, the

faster you’ll earn and the more you’ll have. Investing is the slow boat, so get

on now. For more on the subject of waiting to get started, have a look at

this.

Leave a comment